Sunday, 5th April 2026

Khabor Wala Desk

Published: 31st March 2026, 12:24 PM

Life insurance policyholders are facing an escalating crisis in Bangladesh as unpaid claims continue to rise sharply, exposing severe liquidity constraints and long-standing governance failures within the sector.

One such case is that of Monjur Rahman, who purchased a policy in 2012 from Fareast Islami Life Insurance Company with the expectation of financial security. When his policy matured in 2022, he was entitled to a payout of Tk 11.19 lakh. Despite submitting all required documentation, he is still awaiting payment.

Rahman described repeated delays and administrative hurdles when pursuing his claim. Even in a moment of urgent need, when his father required hospital treatment, he sought partial disbursement but received no support.

Under the Insurance Act 2010, insurers are legally required to settle claims within 90 days of receiving all necessary documents. However, compliance across the sector remains weak.

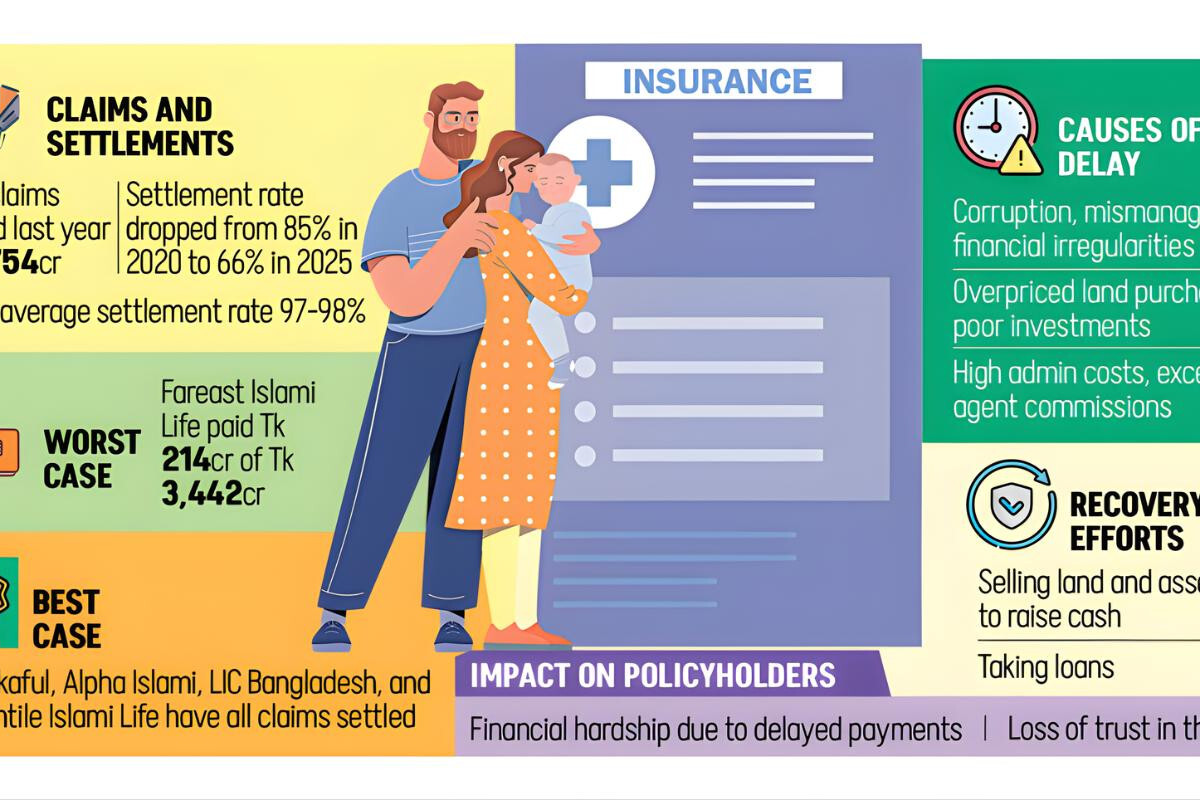

The crisis has worsened significantly in recent years. In 2023, around 10 lakh policyholders were waiting for settlements worth Tk 3,050 crore. By 2025, this figure had risen to approximately 12 lakh policyholders, with outstanding claims reaching Tk 4,403 crore. At least 32 life insurance companies are currently struggling with payment obligations, while seven are reporting particularly poor settlement performance.

Industry-wide settlement performance has deteriorated from 85 percent in 2020 to just 66.06 percent in 2025. This contrasts starkly with global averages of 97–98 percent, and around 98 percent in neighbouring India.

| Company | Claims Filed (Tk crore) | Claims Paid (Tk crore) | Settlement Rate | Policyholders Affected |

|---|---|---|---|---|

| Fareast Islami Life Insurance | 3,442 | 214 | 6% | 5.66 lakh waiting |

| Padma Islami Life Insurance | Not specified | — | 4% | — |

| Progressive Life Insurance | Not specified | — | 21% | — |

| Golden Life Insurance | Not specified | — | 11% | — |

| Sunflower Life Insurance | Not specified | — | 5.5% | — |

| Baira Life Insurance | Not specified | — | 1.6% | — |

| Akij Takaful Life Insurance | — | — | 100% | — |

| Alpha Islami Life Insurance | — | — | 100% | — |

| LIC Bangladesh | — | — | 100% | — |

| Mercantile Islami Life Insurance | — | — | 100% | — |

Regulators and industry experts attribute the worsening situation to a combination of financial mismanagement, corruption, poor investment decisions, excessive administrative costs, and aggressive competition. Several insurers are reportedly attempting to raise liquidity through asset sales, bank borrowing, and recovery plans.

A major audit commissioned by the insurance regulator in 2021 found significant irregularities at Fareast Islami Life Insurance, including alleged embezzlement of Tk 2,367 crore and accounting discrepancies worth Tk 432 crore. The audit also pointed to questionable land transactions and loans secured against financial instruments such as Mudaraba Term Deposit Receipts (MTDRs), which are Shariah-compliant investment accounts designed to generate profit-sharing returns.

Company executives have largely attributed the crisis to historical mismanagement. Fareast Islami Life Insurance’s chief executive acknowledged severe liquidity pressure stemming from past corruption and misappropriation, noting plans to liquidate land assets and seek loans to stabilise cash flow.

Other firms, including Baira Life Insurance and Progressive Life Insurance, cited long-standing governance instability, unprofitable land investments, and weak financial oversight as key contributors to their ongoing difficulties. Some also pointed to operational disruptions following regulatory interventions and political changes in 2024, which they say further constrained liquidity.

Industry leaders have criticised the regulatory environment for failing to enforce the 90-day settlement rule effectively. Experts argue that weak oversight has enabled persistent delays and, in some cases, deliberate withholding of payments.

Economists and insurance academics note that underperformance in investment returns has severely limited insurers’ ability to honour claims. There are also concerns that some companies avoid settlements due to minimal perceived legal consequences.

Without structural reform—such as consolidation of weak insurers, stricter governance enforcement, and wider insurance coverage expansion—the sector risks further erosion of public trust and continued financial instability.

Comments