Monday, 6th July 2026

Khabor Wala Desk

Published: 21st February 2026, 4:49 AM

Domestic banks have emerged as decisive leaders in the financing of the country’s external trade, marking a significant structural shift in the financial architecture of import and export transactions. A decade ago, a substantial proportion of trade-related finance was arranged through foreign institutions, largely due to their established international networks, advanced risk-management frameworks, and technological superiority. At that time, domestic banks faced constraints in foreign exchange liquidity, cross-border compliance systems, and global correspondent relationships, which limited their competitiveness.

Over the past ten years, sustained investment in digital infrastructure, automation of compliance procedures, specialised trade finance divisions, and enhanced foreign currency liquidity management has transformed the competitive landscape. Domestic banks now play a leading role in import settlement, export financing, and the issuance of documentary guarantees. Their strengthened operational capacity has repositioned them at the core of cross-border commercial flows.

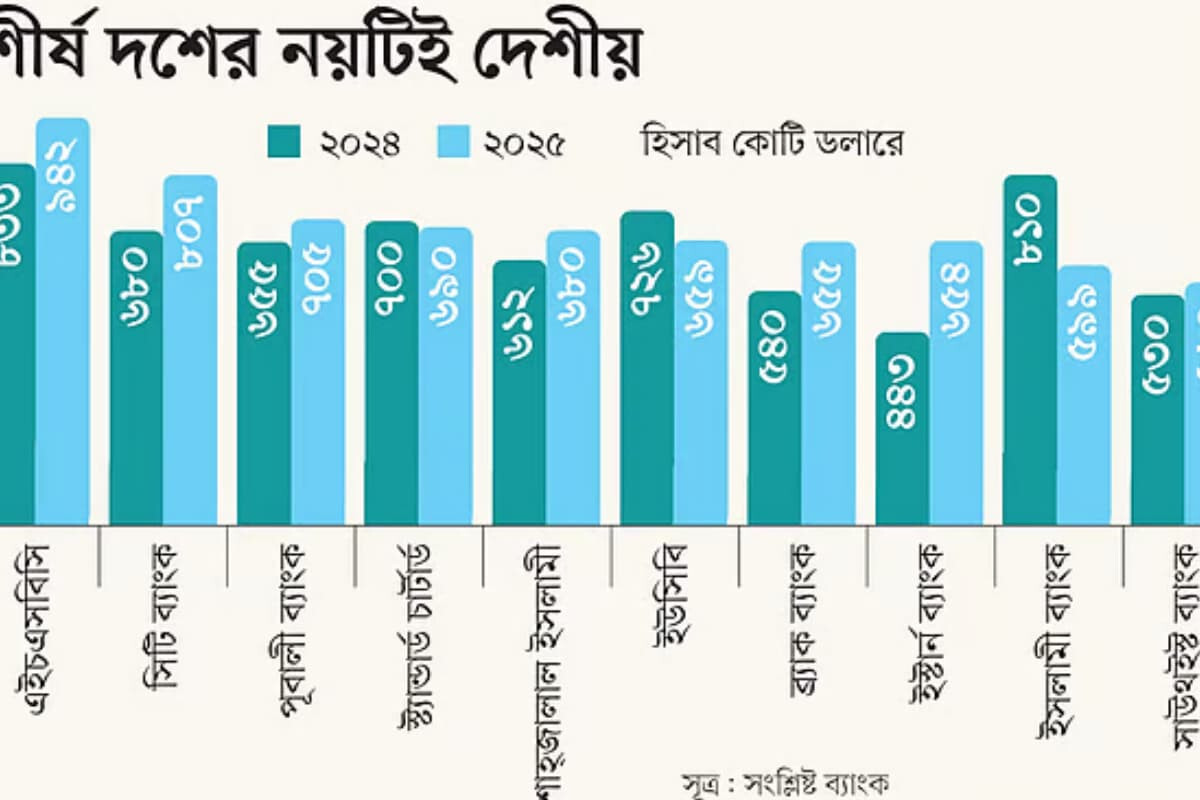

Data for 2025 illustrates this transition clearly. Total trade transactions conducted by leading institutions reveal that domestic banks occupy two of the three top positions by volume. While HSBC remains the largest single player, domestic institutions have narrowed the gap considerably and, in some cases, surpassed foreign competitors in annual growth.

| Bank | 2024 (USD bn) | 2025 (USD bn) |

|---|---|---|

| HSBC | 8.33 | 9.42 |

| City Bank | 6.80 | 8.07 |

| Standard Chartered | 7.00 | 6.90 |

| Shahjalal Islami Bank | 6.12 | 6.80 |

| United Commercial Bank | 7.26 | 6.59 |

| BRAC Bank | — | 6.55 |

| Eastern Bank | — | 6.54 |

| Islami Bank | 8.10 | 6.54 |

| Southeast Bank | 5.30 | 5.60 |

Annual external trade is estimated at approximately 120 billion US dollars, of which nearly 100 billion dollars is channelled through around 20 banks. This concentration underscores the dominance of well-capitalised and technologically advanced institutions in managing the bulk of trade flows.

Several structural factors explain the rise of domestic banks. The adoption of paperless documentation systems, automated compliance screening, faster settlement cycles, and improved foreign exchange liquidity frameworks has enhanced efficiency. Participation in international risk-sharing arrangements and expansion of structured trade finance products have broadened access to global funding lines. Close coordination with the ready-made garments sector has further strengthened transaction continuity and client retention.

Nevertheless, risks remain. Globally, between 80 and 85 per cent of trade transactions are conducted on an open-account basis, increasing exposure for exporters. While trade credit insurance is widely used in advanced markets, its penetration locally remains limited. Broader policy support and wider adoption of modern risk-mitigation instruments could further enhance domestic banks’ participation in regional trade corridors.

Overall, domestic banks have evolved from peripheral participants to central pillars of the country’s external trade finance ecosystem, reflecting enhanced institutional capacity and a recalibrated balance between domestic and international financial actors.

Comments