Thursday, 21st May 2026

Khabor Wala Desk

Published: 21st February 2026, 2:59 AM

A recent analytical review by the central bank has raised serious concerns over the rapid expansion of credit by private commercial banks, warning that excessive lending is generating fresh risks to financial stability. The report identifies a convergence of three principal pressures: lending beyond regulatory ceilings, a persistent rise in non-performing loans, and a deceleration in deposit growth. Together, these factors are constricting liquidity across the banking system and heightening systemic vulnerability.

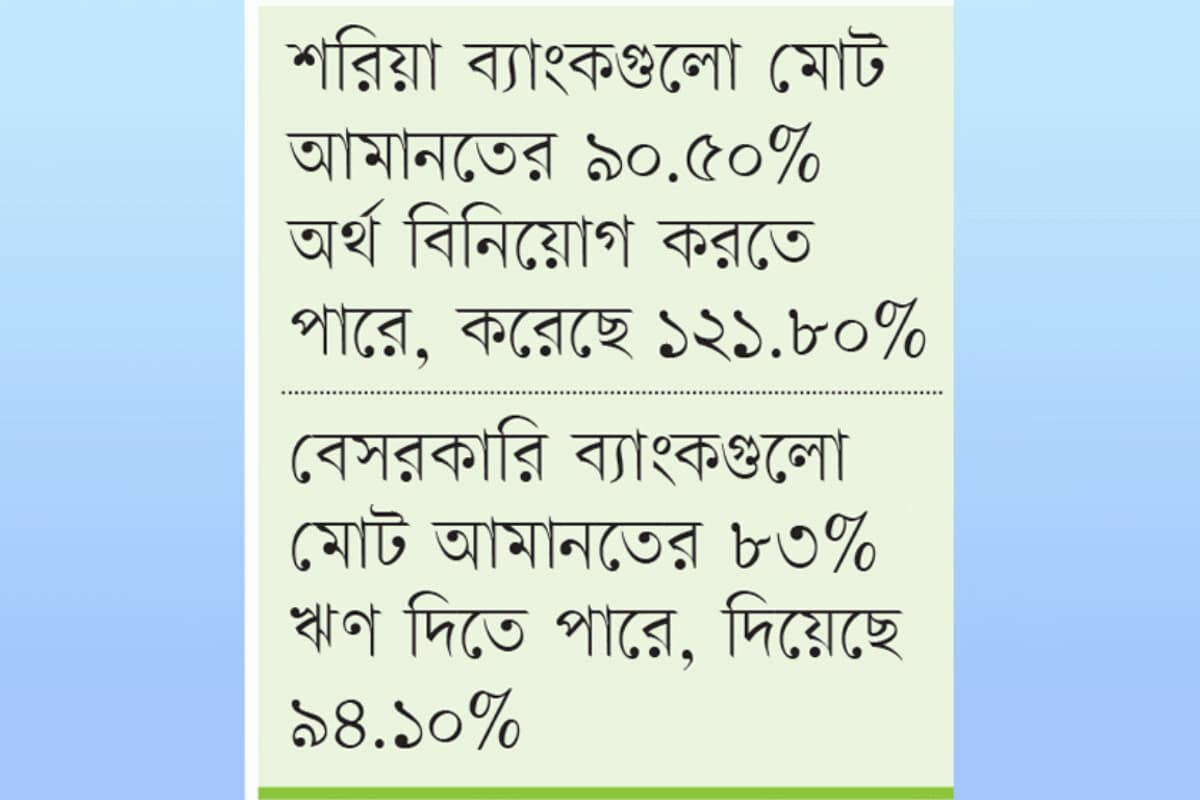

Under prevailing prudential regulations, conventional banks are permitted to extend loans of up to 83 per cent of their total deposits. The remaining 13 per cent must be retained as mandatory reserves with the central bank to safeguard depositor interests. In contrast, Islamic banks operate under a different reserve framework, with a statutory reserve ratio of 9.5 per cent, enabling them to invest up to 90.5 per cent of their deposits. In addition, all banks are required to maintain adequate daily cash balances to facilitate settlement obligations and payment clearances.

However, the report indicates that a significant number of private and Islamic banks have breached these limits. On average, private commercial banks have extended credit equivalent to 94.10 per cent of their deposits—11.10 percentage points above the authorised threshold. The position of Islamic banks appears even more precarious, with an investment-to-deposit ratio of 121.80 per cent, exceeding the regulatory cap by 31.30 percentage points. A substantial portion of this excess expansion has reportedly been financed through interbank borrowing and money market instruments, increasing leverage and refinancing risk.

The comparative position across banking categories is set out below:

| Bank Category | Loan/Investment-to-Deposit Ratio (%) | Regulatory Limit (%) | Deviation (%) |

|---|---|---|---|

| Private Commercial Banks | 94.10 | 83.00 | +11.10 |

| Islamic Banks | 121.80 | 90.50 | +31.30 |

| State-Owned Commercial Banks | 71.70 | 83.00 | –11.30 |

| Specialised State-Owned Banks | 87.00 | 83.00 | +4.00 |

| Foreign Commercial Banks | 55.30 | 83.00 | –27.70 |

The sector-wide average loan or investment ratio currently stands at 86.90 per cent, already above the prudential benchmark for conventional banks. Economists caution that sustained regulatory breaches by specific institutions could destabilise the broader financial architecture. As non-performing loans continue to mount, cash flow pressures intensify, capital buffers erode, and depositor confidence weakens.

Experts further note that when credit growth consistently outpaces deposit mobilisation, banks become increasingly dependent on volatile and often costly funding sources. In periods of market stress, such funding can evaporate rapidly, triggering liquidity shortfalls and contagion effects across interconnected institutions.

To mitigate these risks, analysts advocate stricter supervisory enforcement, rigorous implementation of statutory limits, and a strengthened risk-based capital management framework. Without timely corrective action, the current trajectory of aggressive credit expansion may pose a material threat to medium-term macro-financial stability.

Comments