Saturday, 16th May 2026

Khabor Wala Desk

Published: 28th March 2026, 4:16 AM

Small and medium-sized depositors continue to be the cornerstone of Bangladesh’s banking sector, underpinning both its stability and expansion. Banks have actively adopted digital platforms, simplified account procedures, and various incentives to attract these depositors. Moreover, remittances sent by Bangladeshis living abroad have provided an additional boost, contributing significantly to the rise in bank deposits.

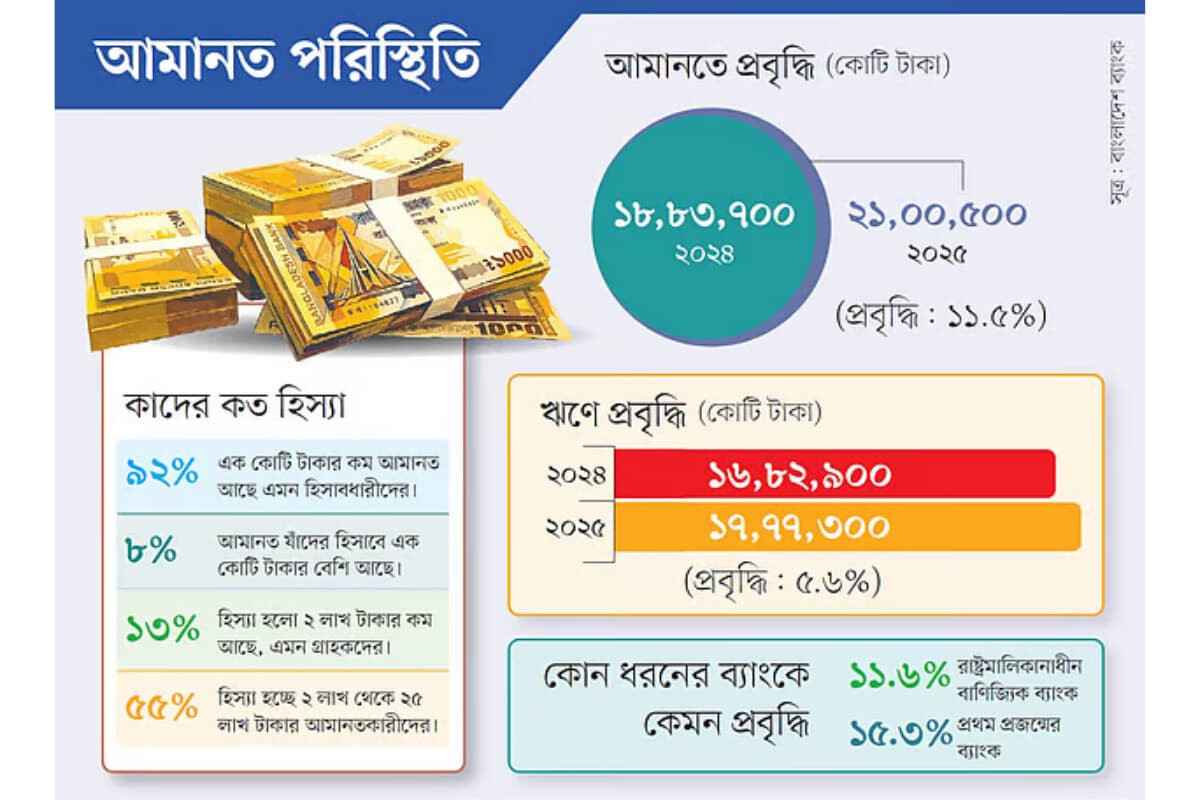

A recent report by Bangladesh Bank shows that 92 per cent of deposit accounts hold less than BDT 1 crore, while only eight per cent of accounts maintain deposits exceeding BDT 1 crore. Notably, 13 per cent of total deposits come from accounts with balances up to BDT 2 lakh, while 55 per cent of deposits are held in accounts ranging from BDT 2 lakh to BDT 25 lakh. This clearly indicates that the country’s banking system largely depends on small and medium-sized savers.

Syed Mahbubur Rahman, former chairman of the Association of Bankers Bangladesh (ABB) and managing director of Mutual Trust Bank, told Prothom Alo, “Banks focus on increasing retail deposits because they are stable and less likely to be withdrawn in large sums. Interest rates are lower on these deposits, making them sustainable. Banks with a higher proportion of retail deposits have a stronger foundation.”

Despite political and economic uncertainties in 2025, total bank deposits increased by 11.5 per cent, while loans grew by 5.6 per cent. Total deposits rose from BDT 18,83,700 crore at the end of 2024 to BDT 21,50,000 crore by the end of last year. Loan disbursements increased from BDT 16,82,900 crore to BDT 17,77,300 crore over the same period.

First-generation private banks and state-owned commercial banks led deposit growth, with first-generation banks recording a 15.3 per cent rise and state-owned banks 11.6 per cent. Household deposits—defined as accounts with up to BDT 1 crore—grew from BDT 10,34,100 crore to BDT 11,80,600 crore, reflecting a 14.2 per cent increase in just one year.

| Deposit Range (BDT) | 2024 (Crore) | 2025 (Crore) | Share of Total | Accounts (Million) |

|---|---|---|---|---|

| Up to 2 lakh | 1,38,100 | 1,56,700 | 13% | 135.9 → 154.8 |

| 2 lakh – 25 lakh | 5,52,200 | 6,52,200 | 55% | 93 → 111 |

| 25 lakh – 50 lakh | 1,37,600 | 1,57,300 | 13% | 3.81 → 4.34 |

| 50 lakh – 1 crore | 1,12,000 | 1,26,000 | 11% | 1.62 → 1.81 |

| Above 1 crore | 83,500 | 83,100 | 8% | 0.035 → 0.038 |

The data demonstrates that smaller savers remain the backbone of the banking sector, with the majority of deposits under BDT 1 crore. This structure not only reinforces the resilience of banks but also provides a stable and sustainable foundation for long-term financial growth.

Comments